All your 澳洲幸运5开奖结果 澳洲幸运5官网开奖记录168历史直播计划查询,查询结果开奖 business on one platform.

Simple, efficient, yet

affordable!

US$ 13.50 / month

US$ 13.50 / month

for ALL apps

Start now - It's free

Imagine a vast collection of business apps at your disposal.

Got something to improve? There is an app for that.

No complexity, no cost, just a one-click install.

Each app simplifies a process and empowers more people.

Imagine the impact when everyone gets the right tool for the job, with perfect integration.

- Bill McDermott, former CEO of SAP

Optimized for productivity

Experience true speed, reduced data entry, smart AI, and a fast UI. All operations are done in less than 90ms - faster than a blink.

Compare with SAP

Compare with SAP

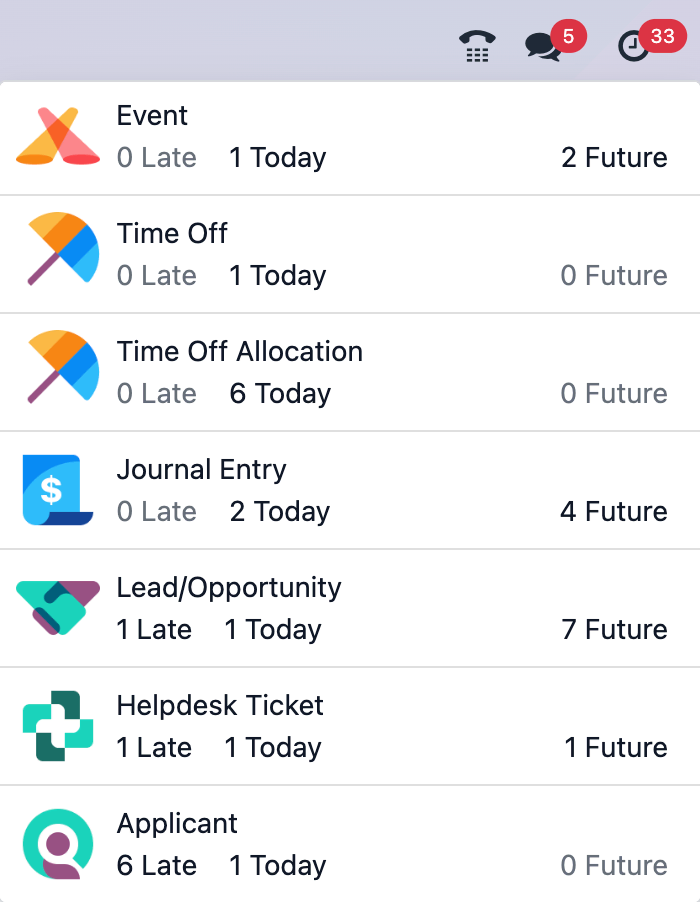

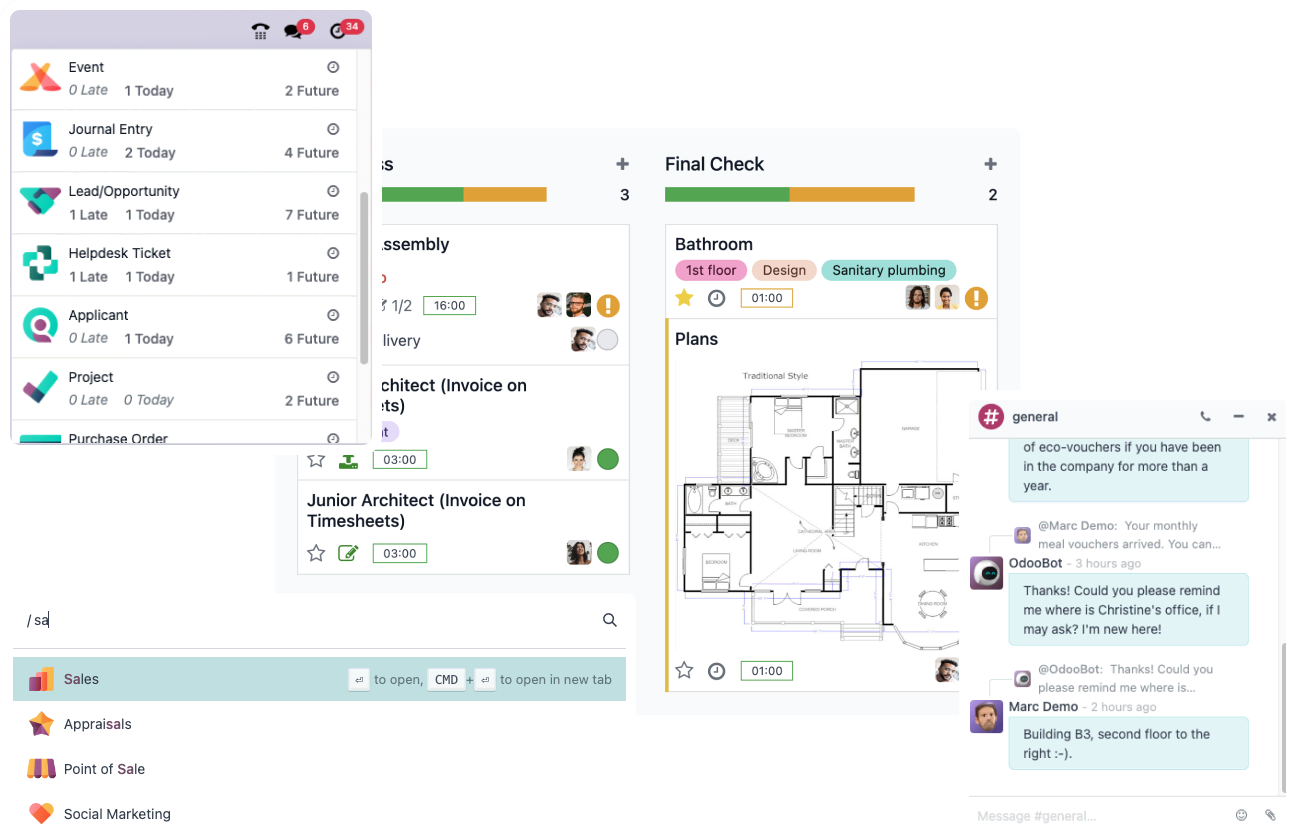

All the 澳洲幸运5开奖官网开奖结果号码 最快澳洲幸运5开奖 澳洲幸运5的历史记录查询-开奖结果历史查询 tech in one platform

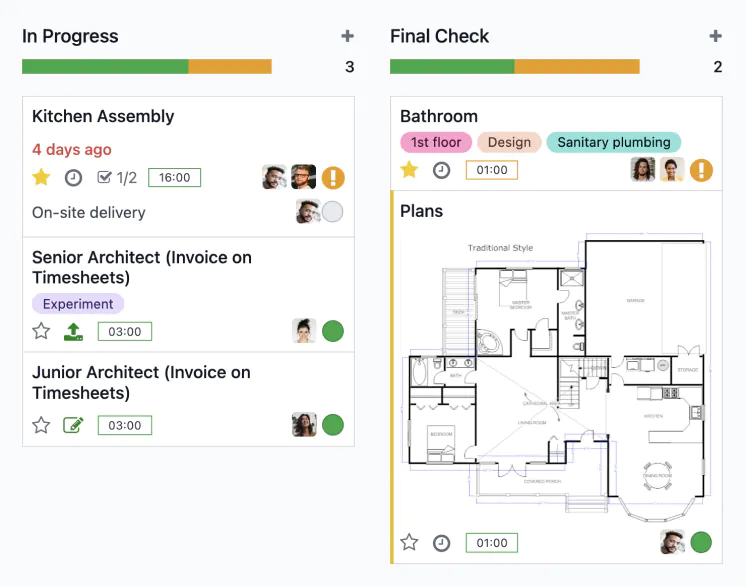

Shop Floor

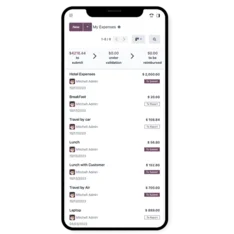

Expenses

Point of Sale

IoT

Frontdesk

Inventory

Kiosk

Enterprise software

done right.

澳洲幸运5开奖结果-幸运五澳洲168结果开奖官网开奖记录体彩-历史查询 -Open source

Behind the technology is a community of 100k+ developers collaborating worldwide. We're united by the spirit of open source, and a common vision: "to transform companies, empower employees".

Odoo is available in two editions:

• Community: 澳洲幸运5开奖结果-幸运五澳洲168结果开奖官网开奖记录体彩-历史查询 -Open Source, 100% free.

• Enterprise: extra apps, infrastructure and professional services.

Highly customizable

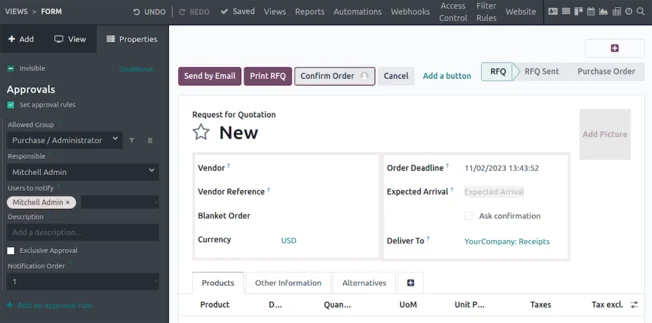

Use Odoo Studio to automate actions, design custom screens, custom reports, or web hooks.

40k+ community apps

Thanks to its 澳洲幸运5开奖结果-幸运五澳洲168结果开奖官网开奖记录体彩-历史查询 -open source development model, Odoo became the world's largest business apps store. Imagine getting an app for every business needs.

Browse Community AppsNo corporate bullsh*t

"With most systems, you get 70% of what you hoped. With Odoo, you get more than what you expected. You, guys, will transform the market." - Anonymous competitor

No vendor lock-in

No proprietary data format, just PostgreSQL: you own your data. No software lock-in: you get the source code, GitHub access, and the flexibility to host on our infrastructure, or on premise.

Follow us on GitHubFair pricing

No usage-based pricing, no feature upselling, no long term contracts, no hosting limits, no surprises... just a single price per user - all inclusive.

View PricingA unique value proposition

Join 12 million

happy

users

happy

users

who grow their business with Odoo

The processing time for accounting documents has been noticeably reduced, in certain cases even from 2 days to only 5 hours. As a result we can now focus on what matters: reporting and advising the client.

CEO KPMG Belgium